I’ve been traveling a bit, which means time for reflection on long plane flights. I’ve also been talking and thinking about management, what it takes to make a small business grow larger, and what it takes to manage teams better. Here’s a list I wrote up in off moments.

- Find people smarter than you are, hire them, and let them run. It’s no coincidence I put this first. You need ideas, interaction, a vibrant, creative environment. If you’re always the smartest person in the room you’re probably delusional, and quite possibly the dumbest.

- Develop ownership inside the team. By ownership I mean being really in charge of something, so you care about whether it works or doesn’t. If you’re key team members don’t swell with pride when things go well and dig in deep to change things when things go poorly, you’re screwed. Do they wait for your lead on everything? Then they don’t own anything, and nothing good is going to happen.

- Embrace mistakes and educated guessing. People afraid of making mistakes can’t operate. If they don’t acknowledge bad results, and don’t care, get rid of them. If they do acknowledge bad results and they bear down to solve problems and do better, make sure they know that you know that. You want people to guess and keep trying. Good decisions have bad outcomes sometimes.

- Improve customers’ lives. Don’t just keep shouting the same old stuff. Find something your team can do that’s good for your customers. Make your customers’ lives better. Do that on your own terms of course, within your own business area.

- Rally the team around the ideas. People will work for something they believe is worth doing because it makes the world better. Believe that, live that, and other people will join you. It’s not about sales growth and profits unless you own the company and plan to sell it. Until then, it’s about doing something that matters.

- Develop a SWOT analysis. It’s pretty simple. Get the team together and do bullet points for strengths, weaknesses, opportunities, and threats. Strengths and weaknesses are internal, opportunities and threats are external. It gets people thinking about strategy.

- Focus the business sharper. You’re probably trying to do too much, too broadly, for a way-too-generalized type of customer. Focus your vision. Bear down hard on something your business can do really well.

- Know the core customer story down to your bones. Your business is a story about doing something people need and want, and doing it better. It’s about helping people. Invent a best-case customer and make her a story in detail. Maybe it’s real, maybe it’s fiction, but it has to feel so real you could script an all-day conversation.

- Find numbers for everybody and live them and own them. Not just dollars in sales or costs or expenses; find the real numbers your team members can live with, take pride in, improve, and (point 2 above) own. That might be page views, clicks, links in, meals served, trips, engagements, conversion, calls, presentations, whatever. Give everybody numbers. Make an environment in which people care about their numbers, check them daily, hurt when they’re bad, feel good when they’re good.

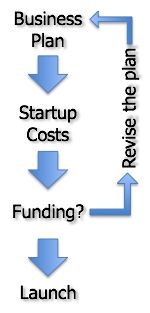

- Plan, step, look, listen, plan, step, and so it goes. It’s a planning process, not just a plan. Start with SWOT, focus on strategy, list assumptions, develop the numbers, and then track, review, revise, and plan again. That’s what we call management.

(Image: istockphoto.com)

(Note: this is the tenth and last of a 10-part series listing my revised top 10 business planning mistakes. The list goes from 10, the least important, to 1, this one, the most important.)

(Note: this is the tenth and last of a 10-part series listing my revised top 10 business planning mistakes. The list goes from 10, the least important, to 1, this one, the most important.) Planning, like steering and management, isn’t just a map and a destination; it’s constant course corrections, the original route map subject to modifications for real time events. So it’s more like a GPS system with real-time traffic and weather information, so you can adjust the route.

Planning, like steering and management, isn’t just a map and a destination; it’s constant course corrections, the original route map subject to modifications for real time events. So it’s more like a GPS system with real-time traffic and weather information, so you can adjust the route.

But that means nothing to the entrepreneur going out into the market with quality goods and services. In the art of positioning, price is the first message you send, and the strongest message.

But that means nothing to the entrepreneur going out into the market with quality goods and services. In the art of positioning, price is the first message you send, and the strongest message. And I’ve written about the displacement principle in small business:

And I’ve written about the displacement principle in small business:

Every business is unique. Your goals, how you define success, your resources, your strategy, your team, your target market, and your business offering are always unique. There’s a post on this blog called

Every business is unique. Your goals, how you define success, your resources, your strategy, your team, your target market, and your business offering are always unique. There’s a post on this blog called

I say let the nature of the business, and the goals of the entrepreneur, determine the financial strategy regarding investment. Some businesses simply can’t sprout without healthy amounts of outside investment. Others have no good reason to even think of investment. And most are in between, with investment a matter of what the owners ultimately want. And there is what I’ve called the

I say let the nature of the business, and the goals of the entrepreneur, determine the financial strategy regarding investment. Some businesses simply can’t sprout without healthy amounts of outside investment. Others have no good reason to even think of investment. And most are in between, with investment a matter of what the owners ultimately want. And there is what I’ve called the  Then in walks somebody who ought to know better saying no, you don’t need to do the plan, just do a pitch.

Then in walks somebody who ought to know better saying no, you don’t need to do the plan, just do a pitch.

You must be logged in to post a comment.