(Note: this is the tenth and last of a 10-part series listing my revised top 10 business planning mistakes. The list goes from 10, the least important, to 1, this one, the most important.)

(Note: this is the tenth and last of a 10-part series listing my revised top 10 business planning mistakes. The list goes from 10, the least important, to 1, this one, the most important.)

Planning is vital for your business. Start with a business plan and a regular review schedule, then track results and changing assumptions and revise the plan as needed to accommodate a changing world. The value isn’t in the original plan, but rather in the planning that follows, which becomes steering your business.

Planning isn’t just a business plan. It’s business management. The real benefit comes from setting up the assumptions and the links between strategy and specific actions, plus the metrics, and the task assignments. As assumptions change – and of course they will – having the plan already in place increases the power of revisions.

Planning, like steering and management, isn’t just a map and a destination; it’s constant course corrections, the original route map subject to modifications for real time events. So it’s more like a GPS system with real-time traffic and weather information, so you can adjust the route.

Planning, like steering and management, isn’t just a map and a destination; it’s constant course corrections, the original route map subject to modifications for real time events. So it’s more like a GPS system with real-time traffic and weather information, so you can adjust the route.

That business plan isn’t the end in itself; it’s just the first step. Expect it to be wrong, and plan to revise it. What you’ll gain is controlling your own business destiny prioritizing, setting up metrics, managing change, and steering your business better.

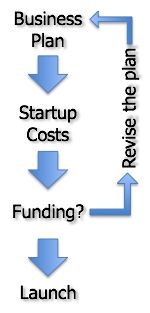

In the illustration: plan vs. actual becomes steering and management.

(image credit: Jiri Hera/shutterstock.com, istockphoto)

But that means nothing to the entrepreneur going out into the market with quality goods and services. In the art of positioning, price is the first message you send, and the strongest message.

But that means nothing to the entrepreneur going out into the market with quality goods and services. In the art of positioning, price is the first message you send, and the strongest message. And I’ve written about the displacement principle in small business:

And I’ve written about the displacement principle in small business:

Every business is unique. Your goals, how you define success, your resources, your strategy, your team, your target market, and your business offering are always unique. There’s a post on this blog called

Every business is unique. Your goals, how you define success, your resources, your strategy, your team, your target market, and your business offering are always unique. There’s a post on this blog called

I say let the nature of the business, and the goals of the entrepreneur, determine the financial strategy regarding investment. Some businesses simply can’t sprout without healthy amounts of outside investment. Others have no good reason to even think of investment. And most are in between, with investment a matter of what the owners ultimately want. And there is what I’ve called the

I say let the nature of the business, and the goals of the entrepreneur, determine the financial strategy regarding investment. Some businesses simply can’t sprout without healthy amounts of outside investment. Others have no good reason to even think of investment. And most are in between, with investment a matter of what the owners ultimately want. And there is what I’ve called the  Then in walks somebody who ought to know better saying no, you don’t need to do the plan, just do a pitch.

Then in walks somebody who ought to know better saying no, you don’t need to do the plan, just do a pitch. No, a business plan isn’t a hurdle you have to get over. That’s just wrong. It’s not a one-time thing. You don’t want to finish your business plan ever. When your business plan is done, your business is done.

No, a business plan isn’t a hurdle you have to get over. That’s just wrong. It’s not a one-time thing. You don’t want to finish your business plan ever. When your business plan is done, your business is done. My first business plan book, written in the late 1990s, carries the title

My first business plan book, written in the late 1990s, carries the title

You must be logged in to post a comment.