(Note: this is the tenth and last of a 10-part series listing my revised top 10 business planning mistakes. The list goes from 10, the least important, to 1, this one, the most important.)

Planning is vital for your business. Start with a business plan and a regular review schedule, then track results and changing assumptions and revise the plan as needed to accommodate a changing world. The value isn’t in the original plan, but rather in the planning that follows, which becomes steering your business.

Planning isn’t just a business plan. It’s business management. The real benefit comes from setting up the assumptions and the links between strategy and specific actions, plus the metrics, and the task assignments. As assumptions change – and of course they will – having the plan already in place increases the power of revisions.

Planning, like steering and management, isn’t just a map and a destination; it’s constant course corrections, the original route map subject to modifications for real time events. So it’s more like a GPS system with real-time traffic and weather information, so you can adjust the route.

That business plan isn’t the end in itself; it’s just the first step. Expect it to be wrong, and plan to revise it. What you’ll gain is controlling your own business destiny prioritizing, setting up metrics, managing change, and steering your business better.

In the illustration: plan vs. actual becomes steering and management.

(Note: this is the ninth of a 10-part series listing my revised top 10 business planning mistakes. The list goes from 10, the least important, to 1, the most important.)

Make no mistake: profits are an accounting story, and cash is real money. You spend cash. Your business dies without it. Profits, on the other hand, depend on the timing on the books of sales and expenses. Following standard accounting guidelines, your sales are likely to be stuff you paid for months ago, that you won’t get paid for for months to come.

It’s November. You could easily be selling things you bought last July, paid for in September, and won’t get paid for until next April. That’s extreme, maybe, but it happens a lot.

All that would show up on the profit and loss would be the sales price, the cost of sales, and the expenses. The profit and loss records the sale when it’s made, not when the supplies are purchased. And it records the sale when it’s made, not when it’s paid for.

Not to mention that your profit and loss doesn’t give a damn about the money you spend to buy new assets, or to pay principal of debt; nor, for that matter, the money you bring in as new debt, or investment. That all happens outside of profit and loss — but it’s vital to cash flow.

So your business planning needs to project profits, yes, but also assets, liabilities, capital, and — by far the most important — cash. The financial calculations behind cash flow can be daunting at first, but they’re still vital. Just as another example, think about this: if you sell to other businesses instead of consumers, then it’s almost certain they’ll expect you to leave them with an invoice and then they’ll wait months to pay. That’s what goes on all the time.

A decent cash analysis will allow for the wait to get paid, and the need to buy things before you sell them, and the need to repay loans and buy new assets and other factors that affect your cash. Make sure you have a reasonable projection of the cash flow.

And if you don’t plan for cash — if you think profits alone will do it — then you can get into real trouble.

(Note: this is the eighth of a 10-part series listing my revised top 10 business planning mistakes. The list goes from 10, the least important, to 1, the most important.)

It’s not that I don’t respect talk about high-level strategy, business models, and business ideas; it’s that the high level strategy-in-the-clouds kind of planning is quite often a waste of time. Nothing but hot air. I’ve written this before, elsewhere, but here it is again:

Good business planning is nine parts implementation for every one part strategy.

And how about this, an old riddle with a business point:

Question: in the classic bacon and egg breakfast, what is the role of the chicken and what is the role of the pig?

Answer: the chicken is involved. The pig is committed.

Good business planning generates commitment. It’s much more about concrete specific details than high-level strategy. It includes dates, deadlines, budgets, forecasts, and specific tasks and responsibilities. It’s about metrics, throughout the business, metrics for everybody, and the practice of following up on metrics to manage performance and the difference between performance and expectations

Does your business plan lists dates and activities and who’s in charge? Why not? Do you track actual results, and the difference between what you planned and what actually happened? Why not?

(Note: this is the seventh of a 10-part series listing my revised top 10 business planning mistakes. The list goes from 10, the least important, to 1, the most important.)

Are you thinking that it’s important to offer better service, or better products, at a lower price? Forget it. That hasn’t been true since the days of Adam Smith and microeconomics and selling lumps of coal.

For lumps of coal, yes, the lower the price, the higher the volume. But that means nothing to the entrepreneur going out into the market with quality goods and services. In the art of positioning, price is the first message you send, and the strongest message.

Markets like the high-priced, high-quality offerings. Don’t be cheap. Low price and low volume works for Walmart and Costco, but they have enormous resources, and you don’t. Price higher, and give more value. Offer high quality, and price accordingly.

Thank goodness this seems to be getting better these days as people become more aware, in general, of the magic of positioning and your price as the first message you send.

(Note: this is the third of a 10-part series listing my revised top 10 business planning mistakes. The list goes from 10, the least important, to 1, the most important.)

It’s just too damn bad that so many entrepreneurs assume to start a business you do a plan, get financed, and then you start. As if the goal of the plan is getting financed; and as if the getting financed is the win, regardless of financed how and by whom and on what terms.

And that’s a big mistake. You should choose investors as carefully as you choose a spouse.

Contrary to the myth, winning the investment isn’t always a win. Getting investment from the wrong people isn’t a win. It’s a recipe for disaster. Marrying your company with incompatible investors can turn a dream into a nightmare. And yet so often when you talk to entrepreneurs they seem to think that just getting that investment is the same as winning the race. Find somebody to say yes and you’ve succeeded.

Not all good businesses make good investments for outsiders. Investors need exits in 3-5 years, while lots of good businesses aim for forever, not just 3-5 years. And entrepreneurs often want independence, while investors usually feel like bosses. They are owners. Some of the best businesses are bootstrapped, meaning they don’t get outside investment. They use their own funds, or early sales, and they grow more slowly but without requiring other people’s money. And some successful businesses are financed by loans, which increases the risk, but doesn’t dilute ownership.

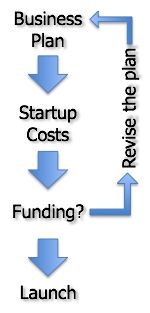

I say let the nature of the business, and the goals of the entrepreneur, determine the financial strategy regarding investment. Some businesses simply can’t sprout without healthy amounts of outside investment. Others have no good reason to even think of investment. And most are in between, with investment a matter of what the owners ultimately want. And there is what I’ve called the Startup Sweet Spot, the natural right level of financing for the startup, based on what it actually needs to develop right, which may or may not require outside funding. As in the diagram here to the right, the plan estimates the ideal startup costs level, and if funding for that isn’t available, then you revise the plan.

The correct goal of the planning process is to help the entrepreneurs determine what their startup really requires, and to help them look at options for growth, so that they can decide whether or not they even have something that will interest investors. And, if they do, then also of course whether or not they want investment. Then, if the entrepreneurs decide they want or need investors, then the planning helps communicate the business to the investors, and that becomes a starting point to deciding whether or not the founders and the investors are compatible.

(Note: this is the second of a 10-part series listing my revised top 10 business planning mistakes. The list goes from 10, the least important, to 1, the most important.)

I’m guessing that the idea of doing a pitch – meaning a slide deck driving a presentation, about 20 minutes’ worth maximum – instead of a business plan is popular mainly because of a huge misunderstanding. People mistakenly think of a business plan as a big honking document, difficult to do, unwieldy, and off putting. So they want to do anything they can to avoid it. Then in walks somebody who ought to know better saying no, you don’t need to do the plan, just do a pitch.

A pitch without a plan to base it on is like a movie without a screenplay. It makes no sense. The pitch is summarizing the plan.

Whether or not you show a plan document to anybody, whether that somebody sees the pitch and not the plan, the plan is your most recent take on what’s supposed to happen, and both the pitch and the document are outputs of the plan. A pitch slide deck summarizes a plan. It doesn’t stand alone.

In the angel investment group I’m a member of, we read summaries first, then watch the pitches that survived the first cut. But nobody gets serious interest without having a business plan, and a pitch without a plan shows up like a sore thumb. As soon as people start asking questions, the pitch alone doesn’t answer them.

The plan itself isn’t a document, or a slide deck, or a memo; it’s what’s going to happen, and why. It’s a combination of strategy and specific steps to implement strategy. It makes the connections between the different functions and relationships in the business. And usually it lives on a computer.

Those documents, the pitch presentations, and the summary memos, even the elevator speech? Those are all just output of the plan.

I’ve decided I need a new top 10 list for business planning mistakes. This isn’t the first I’ve done and I hope not the last either, but it’s a good thing to give these lists a fresh look every so often. And this morning I do a workshop on this topic as part of the Bend Venture Conference in Bend, Oregon; so it seemed like a good time to do it.

I’m doing it like Letterman does, starting with number 10, least important, and counting up to number 1, most important.

No, a business plan isn’t a hurdle you have to get over. That’s just wrong. It’s not a one-time thing. You don’t want to finish your business plan ever. When your business plan is done, your business is done.

A business plan isn’t a thing, like a document, that has lasting value when it’s built. It’s a process. The first plan is the first step in the process. You should review it every month, and revise it as often as your assumptions change.