My Friday video today, from Stanford ECorner, Mike Rothenberg talks about inviting honest feedback. How to ask for it, how to listen, and how people will go slowly at first. You have to reassure them that you really want the feedback.

I’ll add that in my decades in business, I’ve come to treasure the people who give me real feedback. And I’ve noticed that relatively few of us really ask for feedback and then listen to it, and use it. We all say we want it, but most of us want praise more than real opinions, much less constructive criticism. This is a short video, which I post as a reminder.

Or you can click here for the YouTube source video.

Good business management boils down to managing expectations and results. Define expectations clearly, with objective numbers you can track. Track results with the same metrics. Deal with the difference between expectations and results, positive or negative. There’s nothing better than that for developing accountability in a business. And good planning process is the best way to do that.

That’s easy to say, or write, but hard to do. What I’ve seen, in real life, is that every small business owner, or startup founder, has a built-in problem to deal with related to management and accountability. What happens is that in these small groups, co-workers are friends. You roll up your sleeves and work together. And that close collegial relationship, the team mentality, makes it harder to manage well.

Lean business planning sets clear expectations and then follows up on results. It compares results with expectations. People on a team are held accountable only if management actually does the work of tracking results and communicating them, after the fact, to those responsible.

Business management is about what gets measured

Metrics are part of the problem. As a rule, we don’t develop the right metrics for people. Metrics aren’t right unless the people responsible understand them and believe in them. Will the measurement scheme show good and bad performances?

Remember, people need metrics. People want metrics. You and your business need metrics.

Then you have to track. That’s where the lean business plan creates a management advantage, because tracking and following up is part of its most important pieces. Set the review schedules in advance, make sure you have the right participants for the review, and then do it.

Measurement and feedback

In good teams, the negative feedback is in the metric. Nobody has to scold or lecture, because the team participated in generating the plan and the team reviews it, and good performances make people proud and happy, and bad performances make people embarrassed. It happens automatically. It’s part of the planning process. Besides, guilt and fear tactics are the worst kind of fake management.

And you must avoid the crystal ball and chain. Sometimes — actually, often — metrics go sour because assumptions have changed. Unforeseen events happen. You manage these times collaboratively, separating the effort from the results. Your team members see that and they believe in the process, and they’ll continue to contribute.

Do you need to prove a market to investors or bank loan managers? More than ever, good market analysis lives on stories, not numbers. The difference between 10 and 20 million people, as prospects, is minimal. A story of real market need, a solution that a lot of people want, is way better. If you were an investor, which of these cases would pique your interest better:

5 million prospects

Every small business owner doing social media marketing without having a budget to have a dedicated social media person as an employee.

Of course this is a matter of opinion. But what I’ve seen, among angel investors looking at possible investments, is that the story works better than numbers. The investors themselves imagine the size of the market, for themselves, when the story is done right.

Don’t Ignore Market Analysis Numbers

And I don’t mean you should ignore the numbers; but tell the story first. And never leave a market analysis with just the numbers. Granularity and credibility are very important. Investors would much rather hear about a market made up of small business owners who value social media but don’t want to do it themselves than a market of 4.5 million small businesses. For more on this, you might like other posts here including How Startups Estimate Market Size, Stories as Strategy and Will Your Startup Get Angel Investment.

Informed angel investors and judges at business plan contests accept educated guesses easily, but only if the underlying assumptions are laid out openly. The story behind them drives the credibility.

But the Story is Most Important

Fundamentally, at the core, what proves a market is that people will need or want the business offering. It takes enough people to make the market interesting. And it can be a need or want, not necessarily just need. People need gasoline, food, and clothing; but they want status, prestige, self confidence, and image. Make that story believable.

Furthermore, no market numbers are ever exact. They are always guesses about the future and extrapolations of available information. So whether Have Presence determines its total potential market is one million or two, there is no practical difference between these alternative numbers. There is enough market to operate in, and the business will have to win customers one by one.

Numbers and research rarely if ever really validate a market for investors or banks. Sales validate the market. One of the best opportunities for real entrepreneurs, these days, is to put a product idea on Kickstarter.com or a similar site, to show that people will pay money for it when it’s available. This is essentially pre-sales, or commitments to buy, and it’s very convincing.

Other good validators are early sales, market tests, or letters or commitments from distributors and buyers.

Avoid surveys that collect random or anonymous opinions from people about what they say they would buy or what price they would pay. People behave very differently when answering survey questions than when they are actually spending their own money.

Sometimes segmentation itself – dividing a market into meaningful segments – is strategy. I knew a consultant who divided potential small business clients up according to their decision-making process. Small businesses divided into a range that varied from the seat-of-the-pants autocratic owners, on one extreme, to the consensus-with-the-team owners, on the other extreme. And I was consulting with Apple Computer in the early years when they changed their marketing from focusing on the model and power of the device (Apple II, Macintosh, etc.) to the nature of the users (home, classroom, small business, enterprise, government). That changed the marketing overnight.

One new spin on this that intrigues me is something I want to call segmentation by strategic market intersection. But, I confess, I’d like a better tag for this. I haven’t found it in a book or article, I just started using it.

I developed it first for havepresence.com, in its lean business plan, which defines its target market as an intersection of traits of small business owners. Have Presence does social media posting for business owners. Its potential market consists of owners who match three specific traits:

They understand the value of social media;

They want outside help (not doing it themselves, or with an employee);

They have available budget to pay for the service.

I can draw that as a Venn diagram, showing the intersection of various factors, as shown here:

This intersection is also potentially a good example of how market numbers are sometimes educated guesses at best. This one isn’t going to angel investors. However, in a hypothetical pitch for a scalable defensible product, the vast majority of the angel investors I know and work with would accept this definition without having to put hard numbers behind it. They’d understand that the variable of wanting outside help eliminates most businesses with more than 20 or so employees, narrowing the U.S. version of this market to about 5 million with employees and another 25 million without employees. And they’d understand that the variable of having available budget would eliminate most of the 25 million without employees. They wouldn’t demand exact numbers and they would understand that there is a market there. The potential market is clearly big enough to operate in.

And I also mentioned a hypothetical market definition of a business addressing women between 50 and 70 with a minimum income. That’s another intersection.

Finally, I was working recently with a company that wanted to address the needs of entrepreneurs outside the U.S. who had relatively high disposable income and were regular users of social media. That diagram is shown here:

In that case, available information gave these entrepreneurs reasonably good numbers of Facebook and Twitter accounts in various countries. And they had to estimate what percentage of the adult populations of these countries were entrepreneurs; and what percentage of those had sufficient disposable income. The result is their target market.

Disclosure: I have a financial interest in Have Presence (my daughter’s business).

The guy seems callous, selfish, as he dismisses his wive, lover, or child, with frustration. “Don’t you get it?” he asks. “Don’t you know I’m trying to build a business here?” And sometimes there’s the variation, “I’m doing this for you.” And of course there are lots of other versions. Do you recognize that scene, in books, movies, and television dramas? Take my startup advice. Don’t let that be you.

My point is this: Building a business can be all encompassing. You can work on it all day, through all your meals, and into the night. It can be a reason to back out of all your relationships, ignore the other people in your life, ignore your own health, and do nothing else. It’s easy to obsess. There is always a latest problem, and always a new worry. You don’t have time to be home for dinner, or see the kids’ ball game, take the weekend off, or get regular exercise. And there’s even the reinforcement of the pervasive myth that obsession, renamed or disguised as passion, is the right way to do it.

Don’t let this happen to you. It’s an easy trap to fall into, and hard to get out of. It becomes habit. You get used to it. The people around you get used to it. Time goes by and you haven’t taken care of your physical, mental, or emotional health, much less what really matters to people around you.

You rationalize that this is just temporary; it’s going to stop when you get to this milestone or that one. Your life is suspended on the phrase “As soon as … ” And your health goes bad and you lose your people. Years go by. You realize, later, that you’ve a let a bad situation exist for too long.

Ironically, obsession doesn’t even produce better business. It can spoil your business as well as your life. Productivity isn’t as simple as quantity of work; quality of work matters. A half hour of exercise generates an hour of productivity. Keeping a balance with the rest of your life is likely to generate better ideas and better decisions.

Yes, you can read all over the web how to protect your idea. And people are recommending patents, trademarks, copyright, all of which you should do whenever you can. People also recommend contract-like non-disclosure and non-compete agreements too, which is sometimes good advice, sometimes impractical. But eventually all good ideas get copied. Yours will be too. You’re going to have to deal with it.

As I write this I’m wearing a sweatshirt with University of Oregon colors that says “Oregon” on it and also “UO.” But it doesn’t have the logo of the university on it, or the words and fonts that the university copyrighted. And you can’t copyright the name of the state, or the letters U or O. So the university gets no royalties, and the manufacturer owes none.

I should make this clear: I am not saying don’t bother to protect your intellectual property properly. Please don’t misunderstand. Yes, register, apply, take all the steps your attorney recommends. Do what you can. It will help hold competition off and protect your secret sauce for a while. I’m just saying you shouldn’t think you are really protecting from copying, no matter how good your protection is. Smart competitors will get around your intellectual property, even if you manage it correctly and make that as hard as possible. It will still happen eventually.

And here’s my favorite example.

Volkswagen’s new beetle…

Volkswagen Beetle

Volkswagen introduced its new beetle in 1997. What a cool idea that was. It took its looks from the traditional beetle that was immensely popular a few decades earlier, but created a brand new car. What a great idea. And it was commercially successful.

Followed by the new Mini-Cooper…

Mini-Cooper

Not long after Volkswagen’s new beetle, BMW came up with the new Mini-Cooper in 2000. If the old VW was the classic small car success of the 1960s in the U.S. the Mini Cooper S was the darling of the racing magazines at about the same time. It was a tiny British economy car jazzed by John Cooper, famous for formula one racing. BMW bought the British manufacturer and introduced the new Mini.

And then the new Fiat 500

New Fiat 500

So by the time the old VW and the Mini-Cooper had been reborn successfully, Fiat, the Italian auto maker, came up with the same idea for its iconic Fiat 500, which had been the Italian version of the VW during the 1950s and 1960s. That one was released in 2007. It was basically the same idea – take an old standard, a past success, and redesign it for a new car. Buyers like that, and branding is almost automatic. Ride on its history.

The Point is That Copying is Everywhere and All the Time

If you’re successful, people will copy you. You can hold them back with registered patents, trademarks, and copyright, but that’s a delay, not a wall. Volkswagen did not sue BMW for copying its idea, and neither Volkswagen nor BMW sued Fiat. This kind of copying is legal.

In almost any kind of business, from high tech to classic, good ideas get copied. It’s like in fiction, movies, television, fashion, and so many human endeavors. It’s part of life. Laws only protect you so far.

To avoid being run out of time by competitors, you have to stay on top of the business, assume you will be copied, and keep doing what you do well.

Diversity is good for business. Equal opportunity is not only morally and ethically right, it’s also a better way to run a business. Here are some reasons why, and points to consider.

What’s intuitively obvious

It’s pretty much accepted wisdom that when people come together in a common business, it’s better for them to have different skills and experience that the same thing. You want somebody good at sales, somebody good at marketing, somebody who likes managing the money, somebody who can produce whatever it is you sell, right? That’s aside from gender, ethnic, religious, age diversity. The idea is commonly accepted.

Go from there to the obvious parallel with diversity of vision, background, outlook, and experience within a single business culture. Think for just a moment about the larger vision involved in branding and marketing, expansion, and growth. Which is more likely to produce new ideas, early alerts of changes, awareness of new markets and new products: the birds of a feather who flocked together, or a group that includes different people with different backgrounds and ideas?

Diverse companies outperform non-diverse companies by 35%, according to a McKinsey study cited in that post.

Sociologist Cedric Herring found that companies with the highest levels of racial diversity had, on average, 15 times more sales revenue than those with the lowest levels of racial diversity. Herring found that for every percentage increase in the rate of racial or gender diversity, there was an increase in sales revenues of approximately 9 and 3 percent, respectively.

A study at the Kellogg School of Management6 found that diverse teams outperform homogeneous ones because the presence of group members unlike yourself causes you to think differently.

In a Catalyst report called The Bottom Line: Corporate Performance and Women’s Representation on Boards7, researchers found that Fortune 500 companies with the highest representation of women board directors performed better financially than those with the lowest representation of women on their board of directors.

Diversity is good for business

The bottom line, for me, is the bottom line: diversity is not just the future, not just the way the western world is going, not just a natural result of trends and technology, and not just morally and ethically right. It’s also good business.

As I continue with my standard business plan financials series, I turn now to developing the spending budget. True, nobody likes budgets, but the budgeting function is one of the most important to management to keep cash in the bank; and we all know it. In standard business plan budgeting, you look for realism and credibility, with educated guesses. And the point of it is setting it down as a standard so you can track it, review it, and revise as needed.

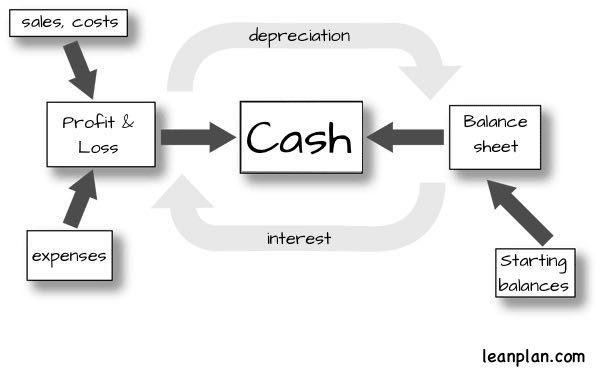

The spending budget is also vital to projected profit and loss and projected cash flow. In the diagram here below of full financials (repeated here from three essential projections posted previously in this series) the spending budget includes both the expenses portion of profit and loss and additional spending that doesn’t show up in profit and loss but does impact the cash flow and balance sheet.

By the way, the word budget, as I use it here, is exactly the same as forecast. The difference between the two is just custom. I could just as easily refer to revenue and spending budgets, or revenue and spending forecasts, as revenue forecast and spending budget. Most people are used to them the way I’m using them, with forecast for revenue and budget for spending.

Also, the difference between Costs and Expenses is significant. In finance and accounting, costs are the direct costs you have in your sales forecast, and expenses are operating expenses like rent, advertising, and payroll. They are not the same thing.

Finally, a special note to our LivePlan users – LivePlan has its own interface to guide you through your spending budget. That’s for a different post. All the concepts you see here are valid, and included with LivePlan – but you don’t have to build them in your spreadsheet.

Three types of spending

There are three common types of spending in a normal business. These are the things you write checks for.

The first is costs, direct costs, what you spend on what you sell. Those are the costs you have already estimated in your sales forecast.

The second is your expenses. They are mostly operating expenses, like rent, utilities, advertising, and payroll.

The third is what you spend to repay debts and purchase assets. I call that “other spending.” These are important financial terms that you have to use correctly; so if you have any doubt, investigate what assets are and how debt repayment is different from interest expense, not an expense, but something that absorbs cash and affects the cash available to the business.

Let’s look first at the most common kind of spending, the operating expenses.

The Expense Budget

Make sure you understand expenses as a technical financial term. Expenses are spending like payroll and rent that aren’t part of direct costs and reduce profits and taxable income. You need to understand that difference if you are going to run a business and manage cash flow. If you have any doubts, please read up on that.

Just as you did for sales forecast and direct costs, try to always project expenses in the same categories you have in your chart of accounts. If your accounting divides marketing expenses into personnel, advertising, and PR, don’t project marketing expenses in your business plan as print, online, and social media. This is important.

Summary of Operating Expenses

Forecasting your operating expenses is a matter of experience, educated guessing, a bit of research, and common sense. Let’s look at a sample expense budget from the same bicycle business plan I used in the sales forecast section above (with middle columns cut out):

All the numbers are educated guesses. Garrett, the bicycle storeowner, knows the business. As he develops his first lean plan, he has a good idea of what he pays for rent, marketing expenses, leased equipment, and so on. And if you don’t know these numbers, for your business, find out. If you don’t know rents, talk to a broker, see some locations, and estimate what you’ll end up paying. Do the same for utilities, insurance, and leased equipment: Make a good list, call people, and take a good educated guess.

Payroll and Payroll Taxes are Operating Expenses

Payroll, or wages and salaries, or compensation, are worth a list of their own. In the case of the bike shop owner, for payroll, he does a separate list so he can keep track. Payroll is a serious fixed cost and an obligation. Garrett’s summary budget (above) has the one line for payroll but it comes from a separate list. He just takes the total into the budget. Here’s the list:

Notice that the totals from the Personnel Plan show up in the expense budget. And if you look closely (it may take a calculator) at the expense row “Payroll Taxes” and compare that amount to the total payroll, you’ll see that it’s an estimate based on 25 percent of payroll. Garrett uses “Payroll Taxes” as a blanket term; it includes what he spends on health insurance and other benefits.

Other spending

This is tricky: standard accounting and financial analysis include only sales, costs, and expenses in the calculation of Profit and Loss. However, in the real world, some of what you spend isn’t included in either costs or expenses. For example, repaying a loan takes money, but doesn’t show up anywhere in the profit and loss. And if you have a product-based business and proper accrual accounting, the money you spend buying inventory doesn’t show up in the profit and loss until that inventory sells. Buying a vehicle or production equipment isn’t tax deductible and isn’t an expense; but it costs money. The rule of thumb is that all expenses are tax deductible, but not all spending is an expense.

What to do? Plan and track your operating expenses for sure. And if you need to handle loan repayments, purchasing assets, distributing profits, owners’ draw, or other spending outside of profit and loss, keep those in your spending budget. Keep track of them. Plan for them.

Understand Starting Costs

Startup costs are a special case that applies to startup businesses only. They are the sum of the assets you need to purchase before you start, plus the expenses you incur before you start. My advice on how to estimate starting costs is coming later, in a separate post.

I believe these three things about startup entrepreneurs, business owners and standard business plan financials:

The essential need-to-know facts about financials are very important;

They are easy enough to learn; and

Bankers, accountants, investors and their analysts expect you to know them and use them correctly.

And here’s why, quoting from a post I wrote for the Amex OPEN forum:

All financial projections are wrong, by definition. We’re human and we don’t predict the future accurately. So don’t expect accuracy. Go for plausibility, and then follow up with regular plan versus actual analysis, review and revisions. We call that management.

What You Need to Know

It starts with standard financial terms. Please don’t use financial terms incorrectly. Banking, finance, and investment assign exact meanings to several important financial terms. They are easy to learn and really important because using them wrongly in business plan financials is at best going to make a very bad impression, and at the worst could even be fraud.

The guardians of financial correctness live in an unforgiving world. Banking and securities laws make even some innocent financial errors look like fraud. Preserving the details of financial standards is the only way business numbers can stand up to legal scrutiny. Numbers in financial statements have to mean what they are supposed to mean.

And seriously, it doesn’t take an MBA degree or CPA certification to know essential financials required for business planning and, really, running a business. It takes focusing your attention for an initial few minutes and then having the discipline to check back when you need to. Read and understand this section, keep it in mind when you deal with financial projections, and you will be fine.

There are three standard financial projections: the Projected Income (also called Projected Profit and Loss), Projected Balance, and Projected Cash Flow. I’m going to continue in following blog posts with more details, and how-to, with steps and illustrations, for each.

All of this is taken from my Lean Business Planning website, reprinted here with permission. If you’d like to jump ahead into the details, you can find it all starting on this page. Or just check back with this blog tomorrow, and once a day for the next few days.

Imagine a bucket of water full to the brim, on a table, right next to a phone and a computer. Now take a brick and drop it into that bucket. Imagine what happens. Water splashes out, right? And that’s probably bad for that phone and computer next to it.

Business Principle of Displacement

That simple story is how I explain the business principle of displacement, in small business, startups, and entrepreneurship. I write it out as:

Principle of displacement: everything you do rules out something else that you don’t do.

The reason this matters so much is that we can’t do everything. So we have to do the most important things. We can’t please everybody. So we have to please the most important, biggest volume groups.

When you decide to add outlier features – used by a few, requested by a few – to a product you are also distracting your team and your product from the main function. And displacement is a legitimate concern as you deal with strategy. Can we expand into schools, from mainly offices? Can we sell to consultants as well as users? In normal growth strategy you have to sort through lots of questions, many possibilities, all with the awareness that you can’t do everything.

Paradox and Strategy

There’s a lot of paradox in managing focus, displacement, and growth.

On the one hand, if you don’t change, you suffer. You can’t just stay focused on the main thing. You have to deal with new possibilities, which sometimes means new products, or new markets.

On the other hand, if you are constantly after the latest shiny new thing, you risk losing focus on what matters most. You don’t want to lose your core while you’re looking to expand.

What I like about real-world business strategy, for startups and small business, is that there is always an other hand.